Roth Conversion ACA Subsidy: Your 2026 Conversion Ceiling

The Roth conversion ACA subsidy interaction is the most powerful — and most dangerous — lever an early retiree can pull in 2026. Every dollar you convert adds a dollar to your Modified Adjusted Gross Income, and the moment your MAGI crosses 400% of the Federal Poverty Level by even a single dollar, you lose every cent of your premium tax credit. That mistake routinely costs FIRE households $10,000 to $30,000 a year, and starting in 2026 there is no repayment cap to soften the blow.

This guide explains how Roth conversions flow into ACA MAGI, what your conversion ceiling looks like by household size, and the exact procedure SubsidyGuard uses to compute the largest conversion you can do without breaking the cliff. Open the calculator and follow along — every example below maps to a setting you can change yourself.

Roth conversion ACA subsidy math: how a conversion changes MAGI

A Roth conversion lands on Form 1040, line 4b as taxable distribution income. That figure rolls up into your Adjusted Gross Income (line 11) with no offsetting deduction, and ACA MAGI is your AGI plus three specific add-backs: tax-exempt interest, non-taxable Social Security, and excluded foreign earned income. None of those add-backs subtract anything, so a $20,000 conversion increases your ACA MAGI by exactly $20,000.

This is the source of the trap. Unlike capital gains (which can be netted against losses), pre-tax IRA contributions (which reduce MAGI), or HSA contributions (also reductive), conversions are pure additive income with no escape valve. The formula is defined in 26 U.S.C. § 36B(d)(2) and operationalized on Form 8962, the form where your subsidy is reconciled at filing time.

If you want to walk through the full MAGI calculation for your own situation, the MAGI calculator breaks it down line by line.

The 2026 conversion ceiling, by household size

Your conversion ceiling is whatever number you can add to all your other income without exceeding 400% FPL. The 2026 marketplace year uses the 2025 HHS poverty guidelines, which set the hard cutoffs below:

| Household size | 400% FPL (cliff) | Typical max conversion if base MAGI is $40k* |

|---|---|---|

| 1 | $62,600 | $22,600 |

| 2 | $84,600 | $44,600 |

| 3 | $106,600 | $66,600 |

| 4 | $128,600 | $88,600 |

*Base MAGI = all other taxable income before the conversion. Real ceilings are higher with HSA, traditional IRA, or solo 401(k) deductions — all three subtract from MAGI.

For most early-retiree households, "base MAGI" is the dividends, interest, capital gains, pension, and (for ages 62+) Social Security benefits that arrive whether you want them or not. Subtract that involuntary income from your 400% FPL line and you have the room left for a conversion. One dollar more and the entire credit reverses.

Why 2026 is harder than 2018-2025

From 2021 through 2025, the American Rescue Plan and Inflation Reduction Act eliminated the cliff entirely — households above 400% FPL still received subsidies, capped at 8.5% of income for the benchmark Silver plan. Those expanded credits expired on December 31, 2025. The original ACA cliff is back as default law.

The 2025 One Big Beautiful Bill Act made the consequences worse in a way most people miss. Before OBBBA, if you accidentally crossed 400% FPL and had to repay advance premium credits on Form 8962, the IRS capped repayment based on your income — a single filer might repay only $1,500 of a $10,000 mistake. Starting with the 2026 tax year, those repayment caps are gone. Cross the cliff and you owe back every dollar of advance credit you received, plus you forfeit any credit you would have claimed at filing. Per analysis of the law, the cliff is now an uncapped clawback for the first time since the ACA's original 2014 design.

This changes Roth conversion planning materially. In 2024, a borderline conversion was a manageable mistake. In 2026, the same mistake is a five-figure tax bill.

The Roth conversion ceiling formula

The conversion ceiling is the largest dollar amount you can convert without breaking the cliff. The math is simple:

Conversion ceiling = (400% FPL for your household) − (all other 2026 MAGI components) − $1 of safety buffer

"All other MAGI components" is everything that hits Form 1040 before the conversion line: wages, self-employment net income, taxable interest, dividends, capital gains, pension distributions, RMDs (if 73+), Social Security (full benefit — the ACA adds back the non-taxable portion), minus above-the-line deductions like HSA contributions, deductible traditional IRA, solo 401(k), and self-employed health insurance.

A naïve approach is to estimate base MAGI, subtract from the cliff, and call that your ceiling. The problem is interaction effects — Social Security taxability changes as MAGI changes, and if you stop short of the cliff but cross 250% FPL, you also lose cost-sharing reductions on Silver plans. The arithmetic looks linear but the policy effects are stepped.

Use the Find max button in SubsidyGuard instead of doing this by hand. It runs a binary search across the cliff, accounting for SS taxability transitions and the cost-sharing reduction breakpoints, and returns the exact maximum conversion that keeps you under the cliff for your inputs.

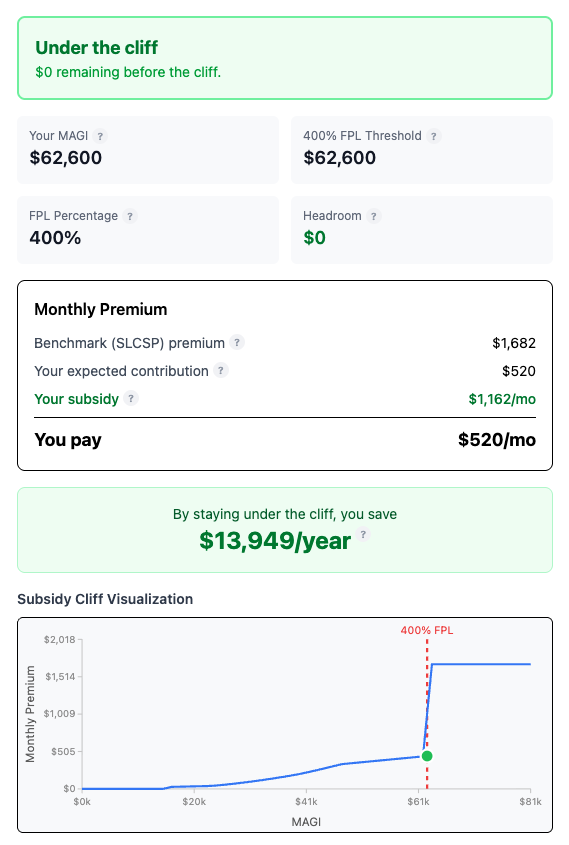

Worked example: 58-year-old couple, $50k in dividends and Social Security

Consider a hypothetical FIRE couple. Both spouses are 58. Their 2026 income consists of $24,000 in qualified dividends, $6,000 in taxable interest, and $20,000 in early Social Security benefits drawn by one spouse. They want to convert traditional IRA dollars to Roth this year to keep future RMDs manageable.

Base MAGI calculation:

| Source | Amount | Notes |

|---|---|---|

| Qualified dividends | $24,000 | Form 1040 line 3a/3b |

| Taxable interest | $6,000 | Line 2b |

| Social Security (full) | $20,000 | ACA adds back the non-taxable portion |

| Subtotal | $50,000 | Before any deduction or conversion |

| HSA contribution | −$8,550 | Family HDHP max for 2026 |

| Base MAGI | $41,450 | Below the cliff with $43,150 headroom |

Their conversion ceiling: $84,600 cliff − $41,450 base − $1 safety = $43,149.

Converting $43,149 keeps them under the cliff and preserves what is likely $18,000-$22,000 in annual premium tax credits at their age. Converting $43,150 wipes out the entire credit and adds the conversion to ordinary-income tax — a single dollar that costs five figures.

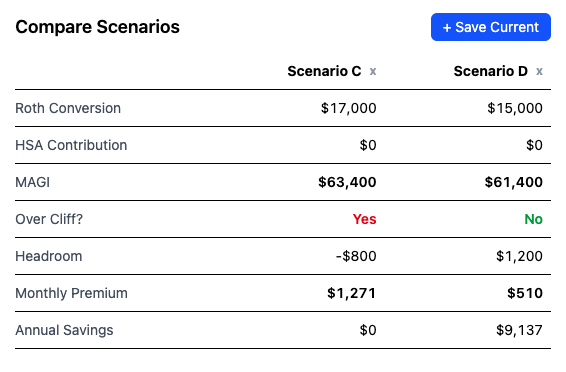

In SubsidyGuard, the scenario comparison tool lets you save this base case, save a second scenario at $43,000, save a third at $50,000, and view all three side by side. The over-cliff column shows a red "Yes" the moment you cross.

The 5-year ladder gap and the ACA trade-off

The classic FIRE Roth conversion ladder converts traditional retirement assets to Roth every year and waits five years per conversion before withdrawing the converted principal penalty-free. The ladder produces tax-efficient retirement income — but only if you can convert enough each year to fill the pipeline.

The ACA cliff caps that pipeline. A single 55-year-old with $40,000 in dividends has only $22,600 of conversion room. A couple with $50,000 in passive income has $34,600. Over a 10-year early-retirement window, that is $226,000–$346,000 in total conversions — often less than what you would want to convert to drain the pre-tax balance before RMDs kick in.

When we built the Find max optimizer in SubsidyGuard, the most common pattern in test scenarios was the ACA ceiling landing 30-50% below what a pure tax-bracket-fill strategy would suggest. A single filer using the calculator to fill the 22% bracket to its top ($50,400) would convert $35,000 — but their ACA ceiling on $25,000 of dividends is $37,600 minus a small safety buffer, leaving almost the same headroom. The numbers happen to align for some incomes and diverge sharply for others; the only way to know which case you are in is to compute both.

There are two ways the math can change:

- Drop ACA, pay full premium, convert aggressively. Makes sense in a single tactical year where the conversion saves more than the lost subsidy.

- Stay under the cliff every year and accept a longer conversion timeline. Slower ladder, lower lifetime tax, full subsidy each year.

SubsidyGuard's annual savings figure tells you what the subsidy is worth in dollar terms for your specific household — usually $8,000-$24,000 — which is what a conversion would need to save in taxes to be worth breaking the cliff.

When converting over the cliff still makes sense

There are real scenarios where exceeding 400% FPL on purpose is the correct call. The three most common:

Low-income years where the cliff sits at a low conversion amount. A 50-year-old single retiree with $5,000 in dividends has a $57,600 conversion ceiling — but if they also need a $30,000 lump sum (medical event, home repair) drawn from a Traditional IRA, they have already eaten most of their headroom. A small additional conversion to fill the 22% bracket may save more in long-term tax than the subsidy costs at that income level.

The last conversion year before Medicare. Aging into Medicare at 65 ends the ACA subsidy entirely. The year before Medicare is the last chance to do an over-cliff conversion without the ACA penalty mattering for the following year.

When the conversion amount eliminates future RMDs. A 63-year-old with $1.2M in traditional IRAs faces RMDs starting at 73 that will push them firmly over 400% FPL anyway. Concentrating conversions in early retirement years, even at the cost of ACA subsidies, may reduce lifetime tax by enough to dwarf 2-3 years of subsidy loss.

FiPhysician's analysis of the ACA-versus-Roth trade-off frames this as "the right answer depends on the size of your traditional balance, your expected retirement length, and the projected tax bracket at RMD age." Run both scenarios in SubsidyGuard before choosing.

How to use SubsidyGuard's Find Max button

The fastest way to find your conversion ceiling for any given year:

- Open SubsidyGuard and enter your filing status, age, household size, and ZIP.

- Enter every income source except Roth conversion: dividends, interest, capital gains, pension, Social Security, wages.

- Enter every above-the-line deduction: HSA, traditional IRA, solo 401(k), SE health insurance.

- Click Find max next to the Roth conversion field. SubsidyGuard runs a binary search and fills in the exact maximum conversion that keeps your MAGI one dollar under 400% FPL for your household.

- Save the result as a scenario. Repeat with different income assumptions — e.g., what if dividends grow 15%, what if you take Social Security one year earlier — and compare scenarios side by side.

The output is the largest defensible Roth conversion for your filing year. It is also the number you give your tax software when estimating Q4 quarterly payments, so the year-end conversion does not surprise your Form 8962 reconciliation.

FAQ

Do Roth conversions count toward ACA MAGI?

Yes — fully and without exception. A Roth conversion appears on Form 1040 line 4b as taxable IRA distribution income, flows into AGI on line 11, and ACA MAGI applies no offsetting deduction. A $20,000 conversion increases your ACA MAGI by $20,000, which can push you over the 400% FPL cliff if you were close.

What happens at tax time if my Roth conversion pushes me over the cliff?

You repay every dollar of advance premium tax credit you received on Form 8962, and you forfeit any credit you would have claimed at filing. Starting in tax year 2026, the repayment caps that previously limited this clawback are gone — the full amount is owed regardless of household income. The IRS treats this as additional tax on your return.

Can I undo a Roth conversion that breaks the cliff?

No. The Tax Cuts and Jobs Act of 2017 repealed Roth conversion recharacterization effective January 1, 2018. Once a conversion completes in a given tax year, it is permanent. This is why running the math before initiating the conversion — not after — is essential.

Should I do a Roth conversion if I'm on an ACA plan?

Often yes, but only up to your conversion ceiling. The subsidy is worth $8,000-$24,000 per year for most FIRE households under 65, which is real money. Convert up to one dollar under 400% FPL every eligible year, fill multiple ladder rungs over a decade, and you capture both the tax-free Roth growth and the full annual subsidy. The wrong move is converting blindly to fill a tax bracket without checking what it does to your subsidy.

Run your own numbers in SubsidyGuard, or read the ACA Subsidy Cliff pillar guide for the broader strategy context.