MAGI Calculator for ACA Subsidies (2026)

Most MAGI calculators online compute the wrong number for health insurance subsidies. The IRS defines MAGI differently for Roth IRAs, Medicare premiums, and ACA subsidies — and the ACA version adds back 100% of Social Security benefits, a rule that trips up thousands of early retirees every year. This MAGI calculator uses the ACA-specific formula so you can see exactly where you stand against the 400% FPL cliff.

Open the free MAGI calculator →

How the ACA MAGI calculator works

The calculator takes your income sources — wages, retirement withdrawals, Roth conversions, Social Security, investment income — and applies the ACA-specific MAGI formula defined in 26 U.S.C. § 36B and IRS Publication 974. Your ACA MAGI equals your Adjusted Gross Income (Form 1040, line 11) plus three add-backs: tax-exempt interest, non-taxable Social Security benefits, and excluded foreign earned income. Nothing else.

Enter each income source individually and see your total MAGI update in real time against the FPL thresholds for your household size. Unlike a simple sum, SubsidyGuard's MAGI calculator isolates every component so you can see marginal impact — which specific dollars are the ones that put your subsidies at risk.

Here is a quick reference for how each income source flows into ACA MAGI:

| Income Source | Included in AGI? | Added Back for MAGI? |

|---|---|---|

| W-2 wages | Yes | — |

| Roth conversion | Yes | — |

| Capital gains (realized) | Yes | — |

| Traditional IRA/401(k) withdrawal | Yes | — |

| Qualified/ordinary dividends | Yes | — |

| Self-employment income | Yes (net of 1/2 SE tax) | — |

| Tax-exempt interest (muni bonds) | No | Yes |

| Non-taxable Social Security | No | Yes |

| Foreign earned income (excluded) | No | Yes |

| HSA contributions (deduction) | Reduces AGI | Not added back |

| Traditional IRA contribution | Reduces AGI | Not added back |

Why "MAGI" means different things for different programs

The IRS uses the term "Modified Adjusted Gross Income" across at least seven different tax provisions, each with its own set of add-backs. A generic MAGI calculator — the kind you find on Omnicalculator or SmartAsset — typically computes MAGI for IRA contribution purposes, which adds back student loan interest, tuition deductions, and foreign income but ignores Social Security entirely.

That's the wrong number if you're checking ACA subsidy eligibility. Here's how the formulas diverge:

| Program | Add-backs on top of AGI |

|---|---|

| ACA premium tax credit | Tax-exempt interest + non-taxable Social Security + foreign income |

| Roth IRA contribution limit | Student loan interest + tuition deductions + foreign income + adoption expenses |

| Medicare IRMAA surcharge | Tax-exempt interest + non-taxable Social Security + foreign income (same as ACA) |

| Net Investment Income Tax | Foreign income only |

ACA MAGI and Medicare IRMAA use identical add-backs but have different income thresholds and wildly different consequences for exceeding them. A 64-year-old retiree one year from Medicare needs to track both — and a generic calculator serves neither (IRS, Modified Adjusted Gross Income).

The ACA MAGI formula, step by step

Your ACA-specific MAGI calculation has four steps. For about 70% of taxpayers, steps 2 through 4 add zero and MAGI equals AGI (UC Berkeley Labor Center).

Step 1: Find your AGI. This is Form 1040, line 11. It includes wages, self-employment income, retirement distributions, Roth conversions, capital gains, dividends, interest, rental income, and unemployment — minus above-the-line deductions like traditional IRA contributions, HSA contributions, and half of self-employment tax.

Step 2: Add tax-exempt interest. Municipal bond interest shows up on Form 1040, line 2a. It's excluded from federal income tax but counts toward ACA MAGI. A $40,000 municipal bond portfolio yielding 3% adds $1,200 to your MAGI that you might not expect.

Step 3: Add non-taxable Social Security. Only 0-85% of Social Security is federally taxable, depending on combined income. But the ACA counts 100%. If you receive $24,000 in Social Security and $14,000 is non-taxable on your 1040, that $14,000 gets added back. This single add-back is responsible for more accidental cliff falls than any other line item. It also creates a feedback loop: more income makes more Social Security taxable, which increases MAGI further, which can push even more Social Security into the taxable range.

Step 4: Add excluded foreign earned income. If you claimed the foreign earned income exclusion on Form 2555, the excluded amount is added back. This affects expatriates and digital nomads buying marketplace coverage during U.S. visits.

ACA MAGI = AGI (line 11)

+ Tax-exempt interest (line 2a)

+ Non-taxable Social Security

+ Excluded foreign income (Form 2555)

The Social Security trap

Social Security benefits receive special treatment in ACA MAGI that catches thousands of retirees by surprise every year. On your federal tax return, anywhere from 0% to 85% of Social Security is taxable depending on your combined income. But for ACA purposes, the marketplace counts 100% of your benefit — every dollar, regardless of what the IRS taxes.

A couple receiving $36,000 per year in combined Social Security might only see $22,000 taxable on their 1040. Their AGI reflects the lower number. But ACA MAGI adds back the $14,000 difference. That invisible $14,000 can be the difference between a $9,600 annual subsidy and zero.

This asymmetry between tax MAGI and ACA MAGI is the single most common reason people accidentally fall off the subsidy cliff. The Healthcare.gov income page confirms this rule but buries it in a list — it deserves its own red banner.

If you are claiming Social Security while buying marketplace coverage, subtract your full Social Security amount from the 400% FPL threshold first. What remains is your budget for all other income sources — conversions, capital gains, and part-time work.

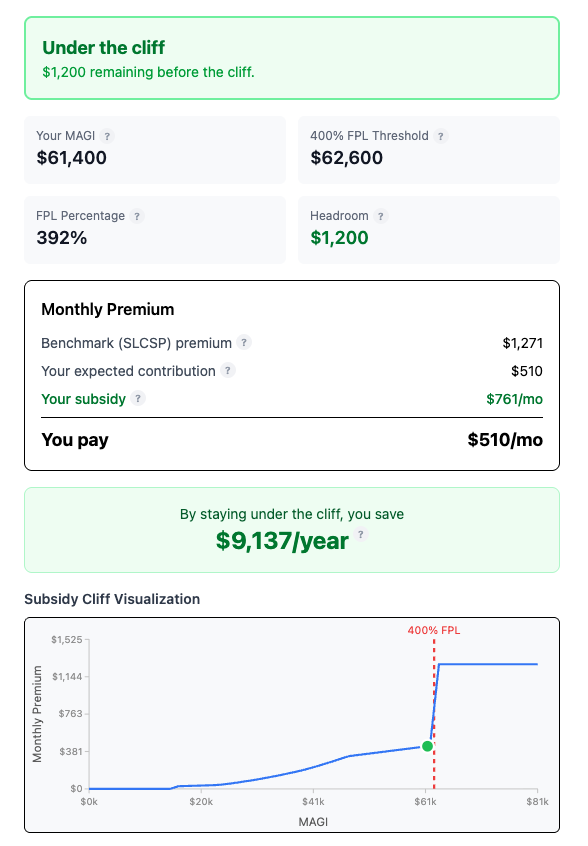

2026 income thresholds: the 400% FPL cliff

In 2026, the enhanced ACA subsidies that ran from 2021-2025 under the American Rescue Plan and Inflation Reduction Act have expired. The original subsidy cliff is back: earn more than 400% of the Federal Poverty Level and you lose your entire premium tax credit. Not the marginal amount — the whole thing. For a 60-year-old, that cliff can mean $10,000 to $22,000 in lost annual subsidies over a single dollar of income (healthinsurance.org).

ACA 2026 coverage uses the 2025 poverty guidelines published by HHS. The "remaining budget" column shows how much room you have for Roth conversions and capital gains after accounting for $30,000 in Social Security:

| Household size | 400% FPL (cliff) | After $30K SS | Remaining budget |

|---|---|---|---|

| 1 | $62,600 | $32,600 | For conversions + gains |

| 2 | $84,600 | $54,600 | For conversions + gains |

| 3 | $106,600 | $76,600 | For conversions + gains |

| 4 | $128,600 | $98,600 | For conversions + gains |

Alaska and Hawaii thresholds are higher. Each additional household member adds $5,500 at 100% FPL. Source: HHS poverty guidelines, applied via thefinancebuff.com.

Your MAGI must fall between 100% FPL (or 138% in Medicaid expansion states) and 400% FPL to qualify for premium tax credits. SubsidyGuard calculates this remaining budget automatically — plug in your Social Security, pension, rental income, and any other fixed sources, and the tool shows exactly how much room you have before you hit the cliff.

Income sources that hit your MAGI — and ones that don't

Early retirees juggle multiple income streams, each with different MAGI treatment. Knowing which ones count is the difference between keeping a $9,600 subsidy and losing it.

Counted toward ACA MAGI:

- W-2 wages and self-employment income (net of 1/2 SE tax)

- Traditional IRA, 401(k), and 403(b) withdrawals — full distribution

- Roth conversions — entire converted amount

- Capital gains (net of up to $3,000 in losses)

- Qualified and ordinary dividends

- Taxable and tax-exempt interest

- 100% of Social Security benefits

- Rental income (net of expenses and depreciation)

- Pension and annuity income

Not counted:

- Qualified Roth IRA withdrawals (contributions and earnings after age 59 1/2 with 5-year rule met)

- HSA withdrawals for qualified medical expenses

- Return of cost basis from taxable accounts

- Gifts, inheritances, and life insurance proceeds

- VA disability benefits

- Loans (margin loans, HELOC, 401(k) loans)

The critical insight: Roth withdrawals are invisible to MAGI. Every dollar converted to Roth today raises MAGI this year but produces MAGI-free income in every future year. For early retirees bridging the gap to Medicare at 65, the math strongly favors converting up to the cliff each year — if you can cover the tax bill without pulling additional taxable income.

Three common MAGI calculation mistakes

The three mistakes that most often push people off the ACA subsidy cliff are using the wrong MAGI formula, ignoring mutual fund capital gains distributions in Q4, and assuming itemized deductions reduce MAGI. Each one is easy to avoid once you know the rules.

1. Using the wrong MAGI definition

A NerdWallet or SmartAsset article about "your MAGI" likely describes the version for IRA contributions, which has different add-backs than the ACA version. The IRS MAGI page lists multiple definitions but does not flag which one applies to which program. Always verify you are using the ACA-specific formula: AGI + tax-exempt interest + non-taxable SS + excluded foreign income.

2. Forgetting mutual fund capital gains distributions

You did not sell anything, but your fund manager did. Actively managed mutual funds distribute realized capital gains in Q4, often in December when you have no time to adjust. A $5,000 unexpected distribution from a single fund can push you over the cliff. Index funds and ETFs generate far fewer distributions — a structural advantage for ACA-conscious investors (Fidelity, MAGI overview).

3. Double-counting deductions that don't affect MAGI

Standard deduction, itemized deductions (charitable giving, mortgage interest, state taxes), and qualified business income deductions reduce your taxable income but not your AGI. Since MAGI starts from AGI, these deductions do nothing for subsidy eligibility. The only deductions that matter are above-the-line: traditional IRA contributions, HSA contributions, half of self-employment tax, and student loan interest. If your strategy relies on a big charitable donation to stay under the cliff, you need a different strategy.

Using the MAGI calculator for Roth conversion planning

Roth conversions are one of the most powerful tools for early retirees — but converting too much in a single year can push you over the subsidy cliff. A disciplined year-end process keeps the math tight.

Here is a four-step approach that works well by November, when most income for the year is already locked in:

- Lock in known income — by November, your W-2, dividends, and realized gains are mostly final

- Estimate December variables — year-end mutual fund distributions, any remaining stock sales

- Set the conversion target — enter increasing Roth conversion amounts until MAGI reaches roughly $2,000 below your FPL cliff

- Build in a buffer — unexpected K-1 income, corrected 1099s, and mutual fund surprise distributions can burn you, so keep at least a $1,500 margin

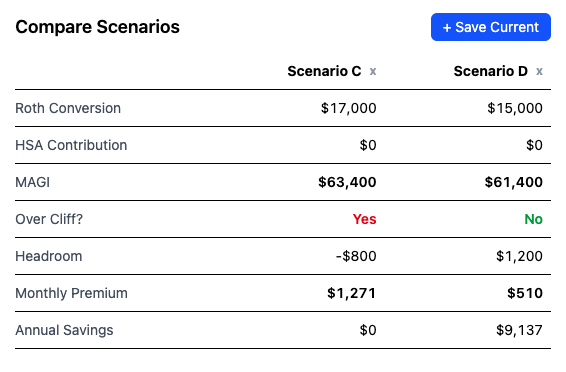

SubsidyGuard lets you save each scenario and compare them side by side, so you can see conversion amounts mapped to subsidy dollars saved before you execute.

Strategies to lower your ACA MAGI

Once you know your number, you need levers to control it. The ACA MAGI formula limits your options to two categories: reduce AGI through above-the-line deductions, or shift income to sources that don't touch MAGI at all.

Above-the-line deductions (reduce AGI directly):

- Traditional IRA contribution: up to $7,000 ($8,000 if 50+)

- HSA contribution (requires HDHP): up to $4,300 single, $8,550 family

- Half of self-employment tax

- Student loan interest (up to $2,500)

Income-shifting strategies:

- Draw from Roth accounts instead of traditional (MAGI-invisible)

- Take margin or securities-backed loans instead of selling assets (no capital gain)

- Harvest capital losses to offset gains (net loss up to $3,000 reduces AGI)

- Delay Social Security to reduce current-year MAGI (and increase future benefits)

- Bunch large Roth conversions into the year you turn 65 and move to Medicare

Each of these strategies interacts with the others. Converting $20,000 to Roth while also taking a $5,000 capital gain and collecting $24,000 in Social Security produces a very different MAGI than any one change in isolation. That's the problem SubsidyGuard solves: enter multiple scenarios side by side and see the cliff impact of each combination before you execute.

Who needs an ACA-specific MAGI calculator?

Generic MAGI tools exist everywhere. An ACA-specific calculator matters if you fit any of these profiles:

Early retirees (pre-Medicare). You're between 50 and 64, living on savings, and buying marketplace insurance. Your income is controllable through withdrawal timing, Roth conversions, and capital gains harvesting. MAGI miscalculation costs you five figures annually.

FIRE community members. You retired early with a portfolio mix of traditional and Roth accounts. You're running a Roth conversion ladder while trying to stay under the cliff. The interaction between conversion amounts and Social Security (if applicable) requires ACA-specific math.

Self-employed with variable income. Freelancers and small business owners whose income fluctuates year to year. A good Q4 can push you over the cliff if you're not monitoring MAGI monthly.

Households with Social Security. Anyone collecting Social Security while on marketplace coverage needs the ACA formula, not the IRA formula. The 100% SS add-back is the single largest source of MAGI surprises.

FAQ

What is the difference between MAGI and AGI?

AGI is your total income minus above-the-line deductions — it's line 11 on Form 1040. MAGI adds certain items back to AGI. For ACA purposes, those items are tax-exempt interest, non-taxable Social Security benefits, and excluded foreign income. For roughly 70% of filers, AGI and ACA MAGI are the same number.

Do Roth conversions count toward MAGI?

Yes — the full converted amount appears in your AGI as ordinary income, which flows directly into ACA MAGI. A $25,000 Roth conversion raises your MAGI by $25,000. The tradeoff: future qualified Roth withdrawals are completely invisible to MAGI, making conversions a powerful long-term strategy for subsidy preservation.

Does the standard deduction lower my MAGI?

No. The standard deduction and all itemized deductions reduce taxable income, not AGI. ACA MAGI is built from AGI, so these deductions have zero effect on subsidy eligibility. To lower MAGI, you need above-the-line deductions: traditional IRA contributions, HSA contributions, or half of self-employment tax.

How do I calculate MAGI if I have Social Security and a Roth conversion?

Start with your AGI from Form 1040 line 11 (which already includes the Roth conversion as income). Then add back the non-taxable portion of your Social Security benefits and any tax-exempt interest. The result is your ACA MAGI. SubsidyGuard's calculator does this automatically and shows how close you are to the 400% FPL cliff.

Do HSA contributions reduce MAGI?

Yes. HSA contributions made outside of payroll are an above-the-line deduction that reduces AGI, and since MAGI starts with AGI, they effectively reduce your MAGI. Payroll HSA contributions reduce AGI through a different mechanism (FICA exclusion) but have the same net effect on your subsidy eligibility.

How much can I earn and still get ACA subsidies in 2026?

Your household income (measured as ACA MAGI) must stay at or below 400% of the Federal Poverty Level. For a single person in 2026, that's $62,600. For a couple, $84,600. Exceed these thresholds by even one dollar and you lose the entire premium tax credit — there's no gradual phase-out under the current law.

What happens if my MAGI goes $1 over 400% FPL?

You lose the entire premium tax credit and must repay it when you file taxes — potentially $10,000 or more depending on your plan, age, and household size. The cliff is binary: there is no gradual reduction. This is why scenario modeling with a tool like SubsidyGuard matters more than a single MAGI estimate.