ACA Subsidy Cliff: The Complete Guide for Early Retirees

The ACA subsidy cliff is the single most expensive mistake early retirees make with their health insurance. Exceed 400% of the Federal Poverty Level by one dollar, and you lose your entire premium tax credit — not just the marginal amount. For a 60-year-old couple, that one dollar can cost $15,000 to $22,000 per year in lost subsidies.

This guide covers the exact income thresholds, what counts toward your Modified Adjusted Gross Income, and five concrete strategies to stay on the right side of the cliff.

What is the ACA subsidy cliff?

The Affordable Care Act provides premium tax credits to help pay for marketplace health insurance. These credits are available to households earning between 100% and 400% of the Federal Poverty Level. The "cliff" is what happens at 400%: your subsidy doesn't phase out gradually — it vanishes entirely.

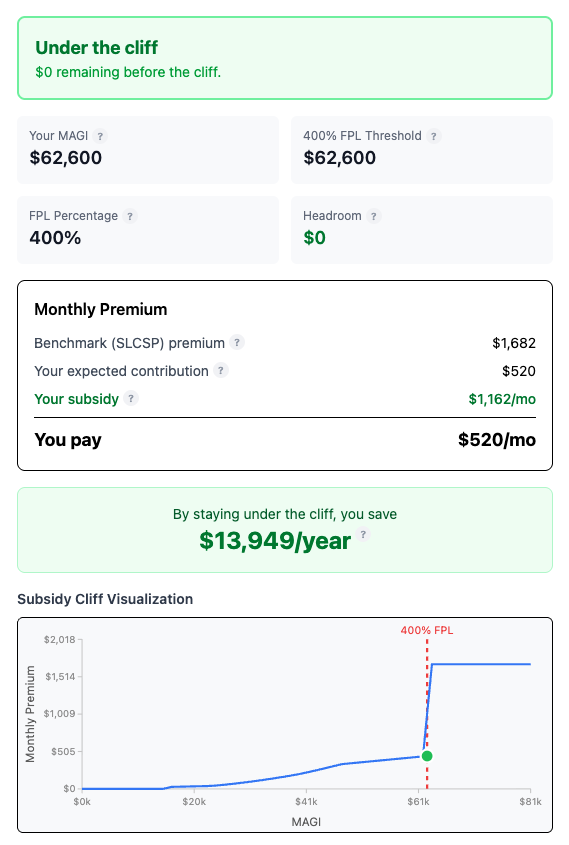

A single filer earning $62,600 qualifies for thousands in annual subsidies. At $62,601, they get zero. The subsidy cliff is the sharpest income threshold in the U.S. tax code, where a single additional dollar of income can trigger a five-figure penalty in lost healthcare subsidies.

Why did the cliff come back?

From 2021 through 2025, the American Rescue Plan Act and Inflation Reduction Act temporarily eliminated the cliff. During those years, households above 400% FPL still received subsidies — they just paid no more than 8.5% of income toward the benchmark Silver plan. Congress did not extend these enhanced subsidies, and they expired on December 31, 2025.

The cliff is not a 2026 event. It is the original ACA structure, written into permanent law in 2010. The 2021–2025 period was the exception. Unless Congress passes new legislation — bipartisan proposals like the CARE Act are under negotiation but have not passed — the cliff applies indefinitely.

If legislation changes, we will update this guide. The income optimization strategies below apply regardless, because even under the enhanced rules, lower MAGI meant larger subsidies.

2026 income thresholds by household size

The ACA subsidy cliff threshold is 400% of the Federal Poverty Level. ACA 2026 coverage uses the 2025 poverty guidelines published by HHS. For 2026, a single filer loses all subsidies at $62,600 and a couple at $84,600 — these are hard cutoffs, not phase-outs. Here are the full thresholds:

| Household size | FPL | 400% FPL (cliff) |

|---|---|---|

| 1 | $15,650 | $62,600 |

| 2 | $21,150 | $84,600 |

| 3 | $26,650 | $106,600 |

| 4 | $32,150 | $128,600 |

Alaska and Hawaii have higher FPL amounts. Single filer cliff: $78,240 (AK), $72,000 (HI). Each additional household member adds $5,500 at 100% FPL.

These numbers shift slightly each year. Check the HHS poverty guidelines for the current year, or use our subsidy calculator to see your exact threshold.

Why early retirees are the most exposed

Early retirees are uniquely vulnerable to the ACA subsidy cliff because they control nearly every dollar of their annual income — IRA withdrawals, Roth conversions, capital gains, and Social Security timing. That control is both the opportunity and the danger.

If you retired before 65 and rely on ACA marketplace coverage as your bridge to Medicare, your income comes from sources you choose: IRA withdrawals, Roth conversions, capital gains harvesting, dividends, and Social Security. Every one of these decisions shifts your MAGI closer to or further from the cliff.

The FIRE community faces this tension constantly. A poorly timed Roth conversion, an unexpected mutual fund capital gains distribution in Q4, or claiming Social Security a year too early can push a household over 400% FPL. The penalty is immediate and binary: you repay the full premium tax credit when you file your tax return.

What counts toward your MAGI (and what doesn't)

ACA subsidy eligibility uses Modified Adjusted Gross Income, which differs from your tax return AGI in one critical way: ACA MAGI includes 100% of Social Security benefits, not just the taxable portion. Most early retirees' MAGI equals their AGI plus non-taxable Social Security — getting this wrong is the most common way people accidentally breach the cliff.

Counts toward ACA MAGI:

- Wages, salaries, self-employment income

- Traditional IRA and 401(k) distributions

- Roth conversions (the converted amount is taxable income)

- Capital gains (including mutual fund distributions you didn't choose)

- Interest and dividends

- Rental income

- Social Security benefits — the full amount, not the taxable portion

- Pension income

Does NOT count:

- Qualified Roth IRA withdrawals

- HSA withdrawals for medical expenses

- Loans against assets

- Gifts and inheritances

- Return of basis from after-tax accounts

The Social Security rule catches people off guard. If you receive $24,000 in Social Security and only $12,000 is taxable on your federal return, ACA still counts all $24,000 toward the cliff calculation. Use our calculator to see exactly where your MAGI lands relative to the cliff.

We built SubsidyGuard after seeing this mistake play out repeatedly in early retirement forums. Posts on r/financialindependence and Bogleheads describe the same story every tax season: someone estimates their MAGI using the taxable Social Security amount from their 1040, plans their Roth conversion around that number, and discovers at filing time that the ACA counted the full benefit. By then the premium tax credit is already spent as advance payments, and the repayment bill runs into five figures.

Five strategies to stay under the cliff

You can stay below the ACA subsidy cliff by controlling which accounts you draw from, timing Roth conversions precisely, maximizing above-the-line deductions, and monitoring for surprise income late in Q4. Here are the five most effective strategies early retirees use, ordered by impact.

1. Optimize Roth conversions to the cliff — not past it

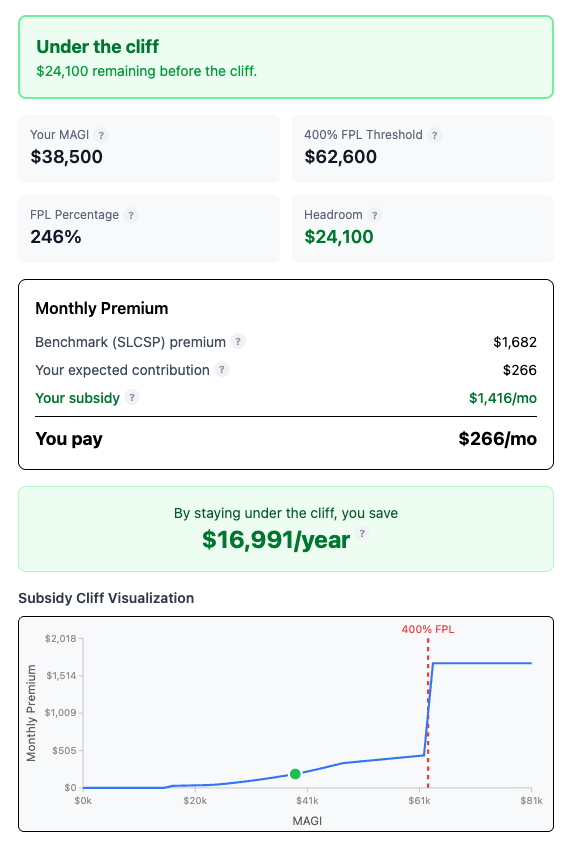

Your SubsidyGuard headroom — the gap between your current MAGI and 400% FPL — is your Roth conversion budget. A single filer with $45,000 in other income has $17,600 of headroom ($62,600 − $45,000). Convert exactly that amount and you stay under the cliff while moving money into tax-free territory.

The conversion itself is taxable income, so it increases your MAGI dollar-for-dollar. Run the numbers before December. Our optimizer calculates the maximum safe conversion automatically.

2. Draw from Roth and taxable accounts strategically

Qualified Roth withdrawals do not appear in your MAGI at all. Neither does return of basis from after-tax brokerage accounts. In years where you need ACA subsidies, pull living expenses from these sources first and leave traditional IRA funds untouched.

A couple needing $80,000 per year could withdraw $50,000 from traditional accounts and $30,000 from Roth — keeping MAGI at $50,000, well under the $84,600 cliff for a two-person household.

3. Maximize HSA contributions

Health Savings Account contributions reduce your AGI dollar-for-dollar, which means they reduce your ACA MAGI too. The 2026 HSA limit is $4,300 for self-only coverage and $8,550 for family coverage, with an extra $1,000 catch-up if you're 55 or older.

You must be enrolled in an HSA-eligible high-deductible health plan to contribute. If your marketplace plan qualifies, this is free MAGI reduction.

4. Delay Social Security if you're under 65

Every dollar of Social Security benefits counts toward ACA MAGI — the full benefit amount, not the taxable portion. Claiming at 62 while relying on ACA subsidies adds $20,000+ to your MAGI that you cannot offset with deductions.

If you can fund living expenses from other sources (Roth, taxable accounts, part-time work below the cliff), delaying Social Security keeps your MAGI lower during your ACA years and increases your benefit amount when you do claim.

5. Watch for surprise Q4 capital gains distributions

Mutual funds distribute capital gains to shareholders in November and December. If you hold actively managed funds in a taxable account, these distributions increase your MAGI whether you wanted them to or not. A $5,000 surprise distribution in December could push you over the cliff with no time to adjust.

Move to index funds or ETFs (which distribute less frequently), hold active funds inside IRAs, or check your fund company's estimated distribution calendar each fall.

The Roth conversion vs. ACA subsidy tradeoff

Staying under the ACA subsidy cliff saves money now, but skipping Roth conversions entirely can cost more in taxes over a 30-year retirement than you save in subsidies. The optimal approach converts up to the cliff each year and occasionally exceeds it when subsidy values are small.

The years between early retirement and Medicare (typically age 55-65) are often the lowest-income years of your life and the most valuable window for Roth conversions. Every dollar you don't convert will eventually face Required Minimum Distributions starting at age 73 -- potentially at a higher tax bracket. Sacrificing all conversions to preserve subsidies can mean paying more in lifetime taxes than you saved.

The right approach is year-by-year: convert up to the cliff in years where subsidies are large, and consider going over it intentionally in years where the subsidy would be small (low benchmark premiums, younger age, or income already near the threshold).

Here is how much a single filer in San Francisco (ZIP 94110) loses at the cliff, by age. These numbers come directly from SubsidyGuard's 2026 SLCSP data:

| Age | Benchmark premium | You'd pay at 400% FPL | Annual subsidy lost |

|---|---|---|---|

| 30 | $647/mo | $520/mo | $1,526 |

| 40 | $728/mo | $520/mo | $2,503 |

| 50 | $1,018/mo | $520/mo | $5,977 |

| 55 | $1,271/mo | $520/mo | $9,013 |

| 60 | $1,546/mo | $520/mo | $12,322 |

| 64 | $1,709/mo | $520/mo | $14,278 |

Couples with both spouses on marketplace coverage face roughly double these amounts. Premiums vary by ZIP — check your numbers.

A 64-year-old loses $14,278 over a single dollar of income. A 30-year-old loses $1,526. Age drives the stakes more than any other variable, which is why the cliff hits hardest in the years between early retirement and Medicare at 65.

Model different scenarios with SubsidyGuard to find the balance that works for your situation.

Frequently asked questions

Does the subsidy cliff apply every year or just 2026?

The cliff is permanent ACA law, not a temporary 2026 provision. It was the rule from 2010–2020, temporarily removed from 2021–2025, and returned in 2026. It applies every year unless Congress passes new legislation.

Can I get subsidies with a large 401(k) but low income?

Yes. ACA subsidies are based entirely on income, not assets. A $3 million portfolio with $50,000 in annual withdrawals qualifies for subsidies. Only the withdrawals (and other income) count toward MAGI.

What happens if I accidentally exceed 400% FPL?

You must repay the full premium tax credit when you file your federal tax return. If you received $12,000 in advance premium tax credits throughout the year and your final MAGI comes in at 401% FPL, you owe back all $12,000. There is no partial repayment above the cliff.

Do any states offer their own subsidies above the cliff?

Several states supplement federal subsidies with their own programs. California, Colorado, Massachusetts, and a handful of others provide state-level premium assistance that may apply above 400% FPL. Check your state marketplace for details.