ACA Income Limit 2026: Thresholds by Household Size

The ACA income limit for 2026 is 400% of the Federal Poverty Level — exceed it by a single dollar and you lose your entire premium tax credit. With the enhanced subsidies expired as of December 31, 2025, this cliff is back in full force for the first time since 2020. For a single filer, the limit is $62,600. For a couple, $84,600. Go over by any amount and you repay every dollar of subsidy at tax time.

If you're an early retiree or FIRE planner managing your own income, check where you stand against the 2026 limit before making withdrawal or conversion decisions.

2026 ACA income limits by household size

The ACA income limit equals exactly 400% of the Federal Poverty Level. For 2026 marketplace coverage, the IRS uses the 2025 poverty guidelines published by HHS — not the 2026 guidelines, which won't apply until the 2027 coverage year. A single filer loses all subsidies at $62,600. A couple — the most common early retiree household — loses subsidies at $84,600.

Here are the complete thresholds for 2026 coverage:

| Household size | 100% FPL (floor) | 400% FPL (cliff) |

|---|---|---|

| 1 | $15,650 | $62,600 |

| 2 | $21,150 | $84,600 |

| 3 | $26,650 | $106,600 |

| 4 | $32,150 | $128,600 |

| 5 | $37,650 | $150,600 |

| 6 | $43,150 | $172,600 |

Each additional person adds $5,500 at 100% FPL ($22,000 at 400%). Alaska and Hawaii have higher thresholds — a single filer's cliff is $78,240 in Alaska and $72,000 in Hawaii.

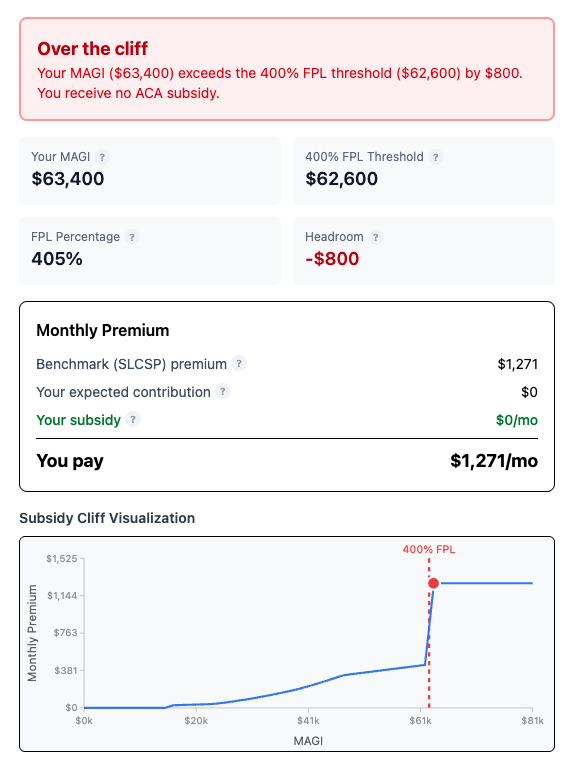

These are hard cutoffs, not phase-outs. Your Modified Adjusted Gross Income must fall between 100% FPL (or 138% in Medicaid expansion states) and 400% FPL to qualify for premium tax credits. For a deeper look at what happens when you cross the line, see our full breakdown of the subsidy cliff.

Source: HHS 2025 Poverty Guidelines

What changed in 2026 — the cliff is back

The original ACA subsidy cliff, written into law in 2010, is back. From 2021 through 2025, the American Rescue Plan Act and Inflation Reduction Act temporarily eliminated the cliff. During those years, households above 400% FPL still received subsidies — they just paid no more than 8.5% of income toward the benchmark Silver plan. Congress let these enhanced subsidies expire on December 31, 2025.

The House passed a three-year extension on January 8, 2026, with 17 Republicans joining Democrats. The bill has stalled in the Senate with no clear path forward. Unless new legislation passes, the cliff applies to every tax year going forward.

The practical impact is severe. CNBC reported in January 2026 that certified financial planner Tommy Lucas of Moisand Fitzgerald Tamayo predicted "astronomical tax bills" starting in early 2027 when 2026 returns are filed. More than 2 million marketplace enrollees have incomes near the cliff threshold. Anyone who received advance premium tax credits and finishes the year above 400% FPL must repay the full amount — potentially $10,000 to $22,000 for older enrollees.

How much subsidy do you get below the limit?

If your income stays below 400% FPL, the government covers the gap between a percentage of your income and the cost of the benchmark Silver plan in your area. The percentage you pay rises with income — someone at 150% FPL pays far less than someone at 350% FPL. Above 400% FPL, the subsidy drops to zero instantly.

Here are the 2026 contribution percentages from IRS Rev. Proc. 2025-25:

| Household income (% of FPL) | You pay (% of income) |

|---|---|

| Up to 133% | 2.10% |

| 133% to 150% | 2.10% to 4.19% |

| 150% to 200% | 4.19% to 6.60% |

| 200% to 250% | 6.60% to 8.44% |

| 250% to 300% | 8.44% to 9.96% |

| 300% to 400% | 9.96% |

| Above 400% | No subsidy — full premium |

These percentages increased sharply from the enhanced-subsidy years. A household at 200% FPL paid roughly 2% of income in 2025 but now pays 6.60% in 2026. The lower your income within the eligible range, the larger your subsidy — which is why precise income management matters. Enter your income to see your estimated subsidy with our calculator.

What counts toward your ACA income limit (MAGI)

ACA subsidy eligibility uses Modified Adjusted Gross Income, not taxable income or take-home pay. Your ACA MAGI equals your Adjusted Gross Income plus three add-backs: tax-exempt interest, non-taxable Social Security benefits, and excluded foreign earned income. For about 70% of filers, MAGI equals AGI. For early retirees, the add-backs are where the traps hide.

Two rules catch retirees off guard repeatedly. First, Social Security benefits count at 100% — the full benefit amount, not just the taxable portion. If you receive $24,000 in Social Security and only $12,000 shows as taxable on your 1040, ACA still counts all $24,000. Second, Roth conversions count as income the year you convert, even though qualified Roth withdrawals are invisible to MAGI. A $30,000 Roth conversion raises your MAGI by $30,000, dollar for dollar.

Capital gains from mutual fund distributions you didn't initiate also count. Your fund manager sells shares in December, and your MAGI jumps — whether you wanted it or not.

For the complete formula and a full table of which income sources count, see our MAGI calculator post. You can also calculate your ACA MAGI directly with SubsidyGuard.

Why early retirees face the highest risk

Early retirees between 50 and 64 face a unique combination of high subsidy value and high income volatility. A 60-year-old couple's benchmark Silver plan can cost $25,000+ per year before subsidies. Losing the premium tax credit at that age means paying the full amount out of pocket — a five-figure swing from a single dollar of income.

W-2 employees have limited control over their MAGI. Early retirees control almost every dollar: IRA withdrawals, Roth conversions, capital gains harvesting, dividend timing. That control is both the opportunity and the danger.

Scenarios that push retirees over the cliff without warning:

- A Roth conversion sized in October that seemed safe gets undermined by a surprise mutual fund distribution in December, pushing total MAGI $3,000 over the limit

- An unexpected K-1 from a partnership investment arrives after year-end, adding income you cannot undo

- Social Security benefits (if claiming early at 62) silently consume $20,000+ of cliff headroom — counted at 100%, not the 50-85% that's federally taxable

- Rebalancing a taxable brokerage account triggers realized capital gains you forgot to plan for

The penalty is binary: full repayment of the premium tax credit when you file. For strategies to stay under the cliff — including Roth conversion optimization and withdrawal sequencing — see our guide to five strategies early retirees use to stay under.

Income limit floor — can you earn too little?

Subsidies require MAGI between 100% and 400% FPL. Below 100% FPL ($15,650 for a single filer in 2026), you receive zero premium tax credits on the marketplace. In the 40 states plus DC that expanded Medicaid, you qualify for Medicaid below 138% FPL ($21,597 single). In the 10 non-expansion states, falling below 100% FPL puts you in the "coverage gap" — too much income for traditional Medicaid, too little for marketplace subsidies.

Early retirees living primarily off Roth withdrawals and loans against assets can accidentally earn too little on paper. If your only taxable income is $10,000 in dividends and you fund the rest of your spending from Roth accounts, your MAGI may be below the floor. The fix: pull enough from a traditional IRA or realize enough capital gains to stay above 100% FPL.

FAQ — ACA income limits 2026

Does a Roth IRA withdrawal count toward the ACA income limit?

No. Qualified Roth IRA withdrawals — contributions at any time, and earnings after age 59 1/2 with the five-year rule met — are not included in gross income and do not count toward MAGI. Roth conversions are different: the full converted amount is taxable income in the year of conversion and raises your MAGI dollar for dollar. This distinction is critical for early retirees running Roth conversion ladders.

Do I count my spouse's income toward the ACA limit?

Yes. ACA household income includes income from you, your spouse (if filing jointly), and anyone you claim as a tax dependent. A dependent child's part-time job income counts toward your household MAGI. For a married couple filing jointly, the 400% FPL threshold is based on a household size of at least 2 ($84,600), not 1.

What if I go over the ACA income limit by a small amount?

You lose the entire subsidy, not a portion. There is no gradual phase-out at 400% FPL. Going $1 over the limit means repaying the full premium tax credit when you file taxes. For a 60-year-old couple on a Silver plan, repayment can range from $15,000 to $22,000 depending on location and benchmark premiums. This is why a $2,000 buffer below the cliff is the minimum margin most financial planners recommend.

Are the 2026 ACA income limits the same in every state?

The FPL thresholds are identical across the 48 contiguous states and DC. Alaska and Hawaii use higher FPL amounts, which means higher income limits. For a single filer: $62,600 (contiguous states), $78,240 (Alaska), $72,000 (Hawaii). Subsidy amounts still vary by state because benchmark Silver plan premiums differ — a $62,000 earner in rural Nebraska gets a different subsidy than the same earner in Manhattan.

We built SubsidyGuard after watching early retirees on Reddit and Bogleheads make the same costly mistake each year — running their numbers through a generic calculator, missing a single income source, and losing their entire subsidy at tax time. Existing tools give you a MAGI number but don't show how close you are to the cliff or let you model what happens if you convert an extra $5,000 to Roth in December. That gap is what SubsidyGuard fills.